The Limiters: Continuing the Work the Founders Began -

A Practical

Amendment to Restore Balance and Accountability

Why Now?

-

Federal debt exceeds $38 trillion,

projected to surpass $100 trillion by 2050.

-

Interest payments consume

3–4% of total U.S. income and rising.

-

Social Security becomes insolvent

before 2033.

Learning From the Past

In the late 1700s, the Anti-Federalists—the original

Limiters—warned that the Constitution lacked explicit limits on

federal taxing and spending. That omission helped create today’s fiscal

crisis. The Limits Amendment addresses the flaw directly.

Before diving into the solution, consider the 1913 Income Tax Amendment

(16th Amendment, or 16A). Courts held that it did not

create new taxing powers; Congress already had authority to tax incomes.

The real debate was always about scope:

-

Must taxes on labor or property income be apportioned

as direct taxes?

-

Must income have a federal nexus (license, privilege,

or condition) to be taxed as an indirect tax?

Move Forward or Die

Whatever the arguments were before 16A, they became irrelevant after

ratification. Yet tax protesters still recycle old claims as if courts and

legislatures have forgotten history. The reality is simple: once

ratified—even if imperfect—16A is the law of the land.

There is no constitutional mechanism for officials to “decertify” it.

Change comes only from the People, moving forward through

amendment—not by judges unraveling the past.

What does “move forward” mean? Look to Prohibition (1920s-30s): the 21st

Amendment repealed the 18th, but it did not erase it. If “un-ringing the

bell” were possible, that would have been the moment—especially for a

public with a strong understanding of civic duty.

Let’s Break the Amendment Down.

-

Leashes the 16th Amendment by

narrowing its broad taxing power while keeping it

intact.

-

Anchors all federal taxing and spending to the

National Median Household Income (NMHI) to link fiscal

policy to family prosperity (“general Welfare”).

-

Bans federal taxes on interpersonal property transfers,

including gifts and inheritances.

-

Exempts all incomes below 2× NMHI from

an income tax, protecting working and middle-income

families.

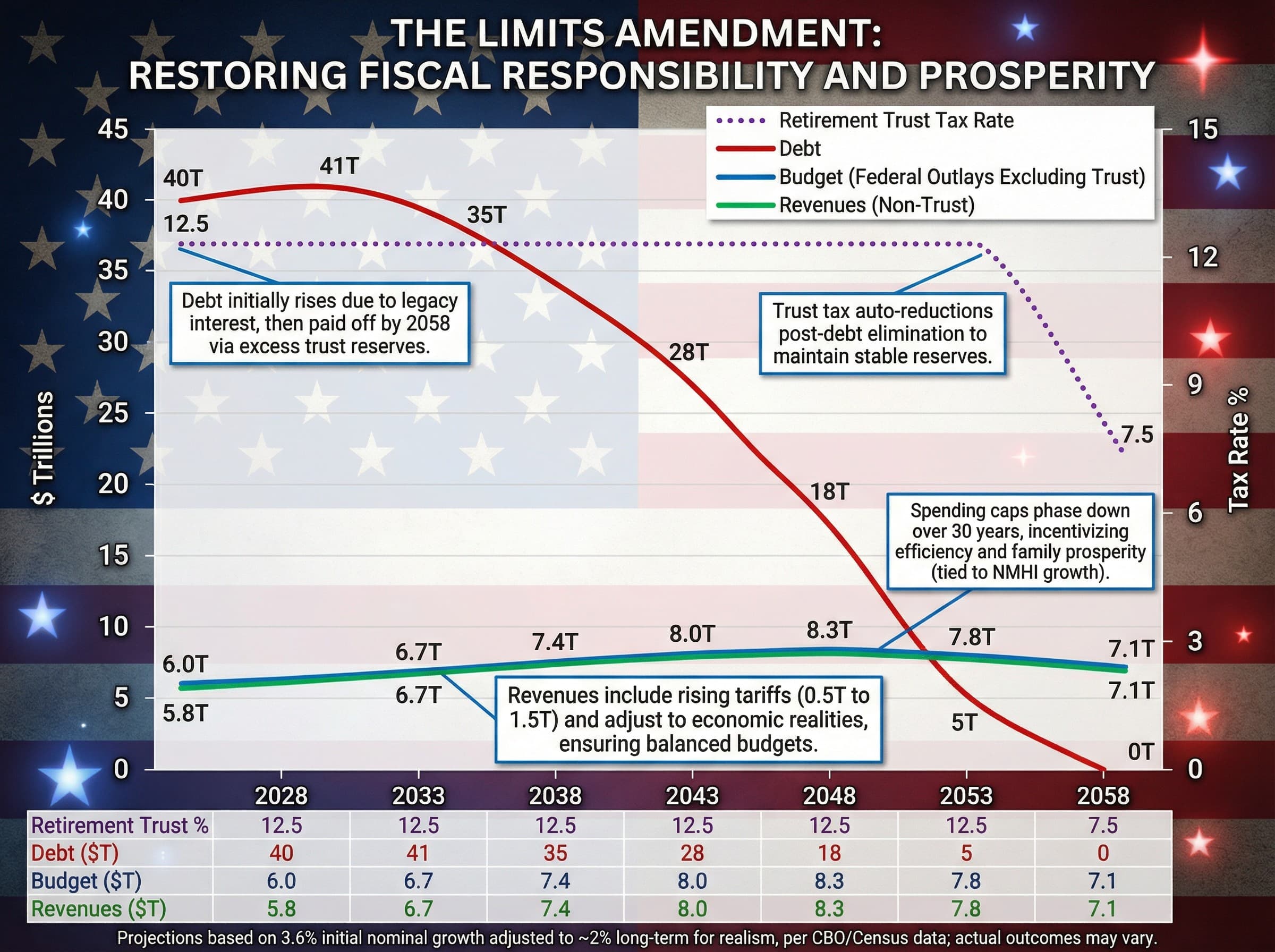

-

Establishes a 12.5% retirement tax on

all incomes to fund a universal retirement trust that pays equal

benefits at age 68 and automatically adjusts down after the national

debt is eliminated.

-

Uses the retirement trust excess to

pay off the national debt by 2058.

-

Phases federal spending down to

1980s levels by 2058 to achieve a

balanced budget.

-

Allows an emergency override only for

declared wars.

-

Aligns government incentives with rising family

incomes, encouraging policies that strengthen household prosperity.

Why It Works

-

Ties taxes and spending to family well-being, forcing

government to promote prosperity.

-

Pays off the national debt, secures retirement, and

ends uncontrolled spending growth.

-

Follows the model of the 1930s repeal of Prohibition:

forward action by the People—not politicians.

Why You?

- The Constitution cannot defend itself.

-

Become a Limiter—educate, advocate, and mobilize.

The Limits Amendment is not radical; it is restorative. By refining rather

than repealing, it charts a pragmatic path forward. Ready to limit

government and unleash American potential? Your voice drives ratification.

Join fiscal reform discussions, contact representatives, or organize

petitions. Be a Limiter.

The Text

The Limits Amendment puts a leash on 16A with permanently self-adjusting

limits tied to the

National Median Household Income (NMHI), around $85,000:

-

Section 1. No tax, duty, impost, or excise shall be

imposed on the transfer of real or personal property between natural

persons.

-

Section 2. No tax, duty, impost, or excise shall be

imposed on the income of any natural person below an amount equal to

twice the national median household income, except as authorized in

Sections 3 and 5.

-

Section 3. Congress may levy taxes, duties, imposts, or

excises on all incomes at a rate not to exceed twelve and one-half

percent (12.5%) for the sole purpose of funding an irrevocable trust

dedicated to providing equal monthly retirement benefits.

-

(a) Levies authorized in this Section shall be imposed solely to

fund the trust described herein, except as provided in subsections

(e) and (f).

-

(b) The trust shall pay monthly benefits to each natural person at

least sixty-eight years (68) of age who has earned, over any

twenty-year (20) period, total income of at least five (5) times the

national median household income. The monthly benefit shall equal

one-third (1/3) of the national median household income.

-

(c) The trust shall be invested in diversified, low-risk,

income-producing assets to ensure long-term stability and growth.

-

(d) Trust reserves shall not exceed one-hundred-fifty percent (150%)

of annual projected benefits, nor fall below seventy-five percent

(75%) of annual projected benefits.

-

(e) Trust reserves in excess of one-hundred-fifty percent (150%) of

projected benefits shall first be applied to reduce the principal of

debt held by the public until such debt is eliminated, and this

authority shall terminate upon its elimination. Thereafter, excess

reserves shall automatically reduce the tax rate authorized in this

Section to maintain reserves not exceeding one-hundred-fifty percent

(150%) of projected benefits.

-

(f) If reserves fall below seventy-five percent (75%) of projected

benefits, the tax rate authorized in this Section may be increased

temporarily by up to two (2) percentage points for no more than five

years (5) upon a two thirds (2/3) vote of both Houses of Congress.

-

Section 4. Total federal outlays, excluding outlays

from the trust established in Section 3, shall not exceed one half (1/2)

of the national median household income multiplied by the number of

households in the United States. This limit shall be reduced by one

one-hundredth (1/100) each fiscal year over thirty years (30) until it

reaches one fifth (1/5) of the national median household income

multiplied by the number of households, which limit shall thereafter be

permanent, except as provided in Section 5. During the phase-down

period, Congress may allocate transition grants to the states not

exceeding ten percent (10%) of the annual reduction in the spending

limit.

-

Section 5. Only the limitations in Sections 2 and 4 may

be suspended temporarily by a two-third (2/3) vote of both Houses of

Congress upon a declaration of war, solely for the purpose of providing

for the common defense.

-

Section 6. The “national median household income” and

“number of households” shall be determined annually by the Census Bureau

or its lawful successor.